Rate cuts should be a tailwind for equities

- 09.20.24

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Economy still on track for a soft landing

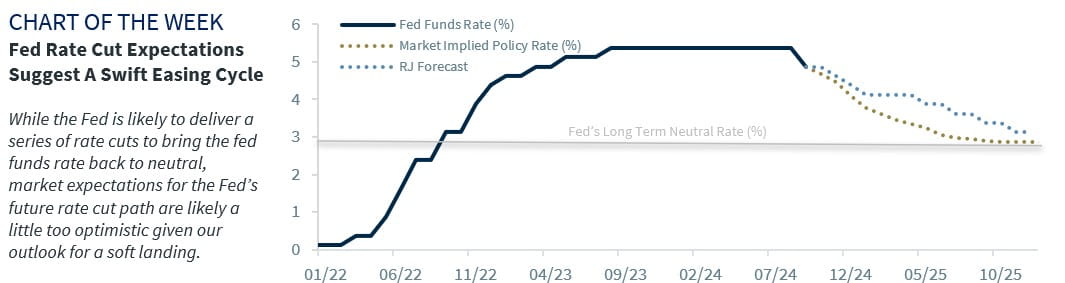

- The bond market is a little too optimistic

- Rate cuts should be a tailwind for equities

The seasons are changing. This weekend marks the autumn equinox—a time of year when the days get shorter, the weather gets cooler, and the leaves start to turn (at least for our friends in the north). While our calendars will show that fall has officially arrived, it may not feel like it as much of the nation will be enjoying unseasonably warm weather. But sure enough, the season will change. And just like nature, where the summer winds down and drifts into fall, monetary policy is experiencing its own ‘change of seasons’ as the Fed transitions into a new easing cycle after the second longest pause period (14 months) in history. The Fed’s rationale: to pre-emptively strike against softening employment conditions to ensure the economy remains on a path to a soft landing. Below we outline our thoughts on what comes next:

- Policy Recalibration Ahead | After much speculation, the Fed kicked off its easing cycle with a large 50 bp cut. The dot plot contained big revisions—signaling an additional 50 bps of cuts in 2024, another 100 bps of easing in 2025 and 50 bps of cuts in 2026, taking the fed funds rate from 5.375% (the mid-point between the 5.25%-5.50% target range) to 2.9% in 2026. While Powell was careful to note that a 50 bp move should not be considered the norm, the Fed’s jumbo sized ‘insurance’ cut was taken to ensure the economy continues to expand at a solid pace and employment conditions do not deteriorate further. This was the first of many cuts that will ultimately bring the fed funds rate back down to a neutral setting (i.e., a rate that neither stimulates or restrains growth—which the Fed upgraded to 2.9% in the latest dot plot). While the dot plot provides a road map, policymakers can move as “fast or slow” as needed depending on the evolution of incoming data. Back to watching the jobs data we go!

- Economy Still On Track For A Soft Landing | While the Fed still faces a tough balancing act, it does appear that policymakers are on track to achieve a rare soft landing for the economy. In fact, the last soft landing occurred in 1995—nearly three decades ago! And while the economy has climbed a wall of worry after the biggest inflation surge and the most aggressive tightening cycle since the 1980s, the Fed is on the cusp of bringing inflation back under control (PCE inflation fell from a peak of 7.1% to 2.5%) without experiencing any significant job losses or a recession. Thus far, that is. Looking at the Fed’s updated projections, a soft landing appears to be within reach. If the economy evolves as the Fed expects—inflation drops to 2.3% and 2.1% in 2024 and 2025, the unemployment rate peaks at 4.4% in 2024 and holds steady in 2025 and growth stabilizes at 2.0% for the foreseeable future—a soft landing can be achieved. Of course, a lot has to go right for this to happen, but this aligns with our outlook as well.

- Bond Market A Little Too Optimistic? | A lot of good news was priced into the bond market heading into the Fed’s FOMC decision. With inflation falling faster and the unemployment rate rising more than the Fed expected, the bond market moved ahead of the Fed’s easing cycle—a textbook reaction. This drove Treasury yields sharply lower as the market priced in a relatively aggressive rate-cutting cycle with a terminal rate of about ~2.8% by year-end 2025 (much sooner and a tad lower than the Fed’s estimates). This pulled Treasury yields lower across the curve, with the policy-sensitive 2-year Treasury yield falling nearly 190 bps below the fed funds rate (before the Fed’s rate cut), down a whopping 112 bps since quarter end—a move rarely seen outside recessions! Given the sharp moves in Treasury yields over the last few months, we believe the bulk of the move is largely behind us and that yields, longer-maturity yields in particular, are not likely to move significantly lower absent a material weakening in the economy (still not our base case).

- Rate Cuts Should Be A Tailwind For Equities | The combination of Fed easing, and a soft landing should prove to be a tailwind for risk assets (equities in particular). Historically, Fed easing cycles have been positive for the equity market. In fact, the S&P 500 has been up ~5% on average in the 12 months following the Fed’s first cut. However, results can vary depending on the trajectory of the economy. If there is a recession, the S&P 500 has been down ~2% on average; if the economy does not enter a recession (e.g., a soft landing), the S&P 500 has been up ~18% on average. The main reason: better economic growth is supportive of higher earnings and justifies the typical path higher. With a soft landing remaining our base case, the Fed cutting interest rates supports our long-term optimistic equity view and a continuation of the bull market. One point to note is that equities (S&P 500) did very well during the last 14-month Fed pause period. Over this period, the S&P 500 rallied ~24%, well above the historical average of ~8% during previous Fed pauses. And rallying is important, as the S&P 500 has only been positive 63% of the time. The bottom line: with the S&P 500 rallying to record levels and currently at some of the most expensive valuations (23.5 LTM P/E) that we have seen in history, there is not much room for disappointment if the soft-landing scenario were to falter.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.